The UAE introduced corporate tax under Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses, administered by the Federal Tax Authority (FTA). This guide covers every aspect of UAE corporate tax: who it applies to, the rates, registration, filing deadlines, free zone rules, small business relief, allowable deductions, and how to file your return on EmaraTax. All information is based on current FTA legislation and official guidance.

1. Overview of UAE Corporate Tax

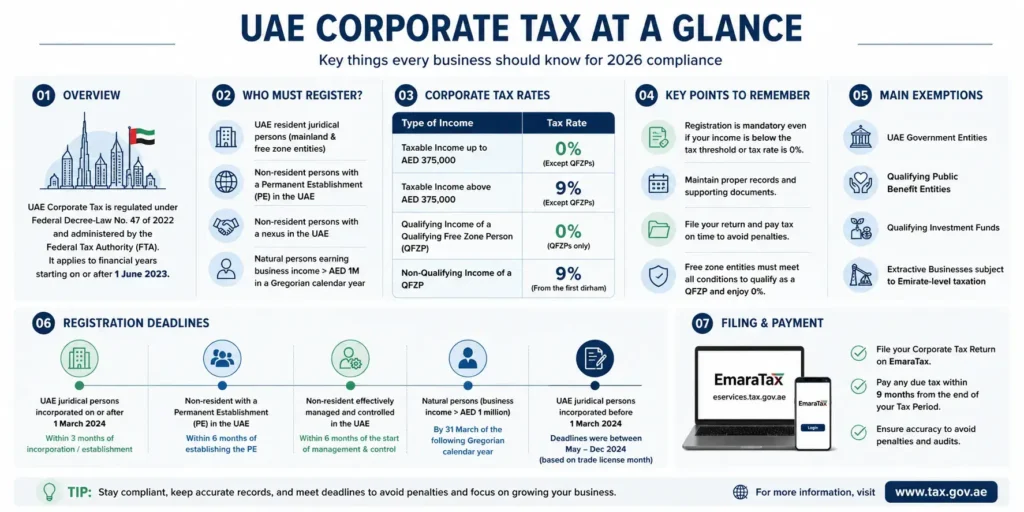

Corporate tax in the UAE applies to financial years starting on or after 1 June 2023. The regime is governed by Federal Decree-Law No. 47 of 2022, supplemented by a series of Cabinet Decisions and Ministerial Decisions issued by the Ministry of Finance and the FTA.

The FTA is the competent authority responsible for administering, collecting, and enforcing corporate tax across all emirates. All registration, filing, and payment is conducted through the EmaraTax portal.

The UAE corporate tax regime applies to mainland businesses and, with important distinctions, to free zone entities. Certain categories of person are exempt from corporate tax under Article 4 of the Decree-Law, including UAE government entities, qualifying public benefit entities, qualifying investment funds, and businesses engaged in the extraction of natural resources that are subject to emirate-level taxation.

Official Source

The primary legislation is Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses, available in full on the FTA legislation page and the Ministry of Finance website.

2. Who Must Register for UAE Corporate Tax

The following categories of person are required to register for corporate tax with the FTA:

- UAE resident juridical persons: All companies incorporated or otherwise formed in the UAE, including limited liability companies, joint-stock companies, and other legal entities.

- Free zone entities: All free zone companies must register and file annual corporate tax returns, even if they qualify for the 0% rate as a Qualifying Free Zone Person.

- Non-resident persons with a permanent establishment in the UAE: Foreign companies or individuals that have a fixed place of business or are otherwise deemed to have a permanent establishment (PE) in the UAE under Article 14 of the Decree-Law.

- Non-resident persons with a nexus in the UAE: Non-residents earning income from the UAE that meets the conditions set out in Cabinet Decision No. 56 of 2023.

- Natural persons: Individuals conducting business activities in the UAE whose total business income exceeds AED 1 million in a Gregorian calendar year are treated as taxable persons and must register.

Important: Registration is mandatory even where the business qualifies for a 0% tax rate, elects Small Business Relief, or expects to have no taxable income. The FTA requires every taxable person to be registered before filing a return.

Software & Experts Together!

New Way to Manage Corporate Tax in UAE

Just scan your invoices and our team will handle all your compliance process inside your mazeed account.

3. UAE Corporate Tax Rates

Under Article 3 of Federal Decree-Law No. 47 of 2022, UAE corporate tax is charged at the following rates:

| Taxable Income | Corporate Tax Rate | Applies To |

| AED 0 to AED 375,000 | 0% | All taxable persons except QFZPs |

| Above AED 375,000 | 9% | All taxable persons except QFZPs |

| Qualifying income of a QFZP | 0% | Qualifying Free Zone Persons only |

| Non-qualifying income of a QFZP | 9% | Qualifying Free Zone Persons only |

Note for Free Zone Entities

The AED 375,000 threshold applies to taxable persons subject to the standard CT regime. It does not apply to QFZPs for non-qualifying income.

4. How to Register for UAE Corporate Tax

Corporate Tax Registration Deadlines

Registration deadlines vary by entity type, as established by FTA Decision No. 3 of 2024:

| Entity Type | Registration Deadline |

| UAE juridical persons incorporated before 1 March 2024 | Deadlines ran from May to December 2024 based on trade licence issuance month (per FTA Decision No. 3 of 2024). These have now passed. |

| UAE juridical persons incorporated on or after 1 March 2024 | Within 3 months of the date of incorporation or establishment |

| Non-resident with a permanent establishment in the UAE | Within 6 months of establishing the permanent establishment |

| Non-resident effectively managed and controlled in the UAE | Within 6 months of the start of management and control |

| Natural persons (business income exceeds AED 1 million) | By 31 March of the following Gregorian calendar year |

Any business that was required to register by 2024 and has not yet done so is already exposed to an administrative penalty of AED 10,000 for late registration. The FTA previously offered a penalty waiver to businesses that filed their first corporate tax return or annual declaration within seven months of the end of their first tax period. Businesses in this position should seek professional advice promptly.

Corporate Tax Registration Process on EmaraTax

How to register for Corporate Tax on EmaraTax

1- Access EmaraTax via UAE Pass

Go to eservices.tax.gov.ae and log in using your UAE Pass credentials. UAE Pass is required for all FTA portal access.

2- Create or access your taxpayer profile

If your entity is already registered for VAT, your existing taxpayer profile will be available. For new registrations, create a new entity profile with full legal entity details including trade licence number, legal form, and ownership structure.

3- Initiate corporate tax registration

Within your taxpayer dashboard, navigate to the corporate tax module and begin the registration application. You will be required to provide entity details, financial year end date, and information on related parties.

4- Upload supporting documents

Prepare and upload your trade licence, memorandum of association, Emirates ID of authorised signatories, and any other documents requested by the portal.

5- Submit and receive your Tax Registration Number (TRN)

Once the application is submitted and approved by the FTA, you will receive a corporate tax Tax Registration Number. This TRN must be included on all corporate tax returns and correspondence with the FTA.

5. Filing Deadlines for 2026

Under Article 53 of Federal Decree-Law No. 47 of 2022, every taxable person must file a corporate tax return within nine months from the end of the relevant tax period. The tax payment is due by the same date. Filing the return without paying the liability, or paying without filing the return, both constitute non-compliance.

The FTA has confirmed that it does not grant general extensions to corporate tax filing deadlines. The September 2025 FTA press release reiterated that “all Corporate Taxable Persons, regardless of the level of income, have a legal obligation to file their Tax Returns.”

| Financial Year End | Tax Period | Filing and Payment Deadline |

| 31 December 2024 | 1 January 2024 to 31 December 2024 | 30 September 2025 (passed) |

| 31 March 2025 | 1 April 2024 to 31 March 2025 | 31 December 2025 (passed) |

| 30 June 2025 | 1 July 2024 to 30 June 2025 | 31 March 2026 |

| 31 December 2025 | 1 January 2025 to 31 December 2025 | 30 September 2026 |

| 31 March 2026 | 1 April 2025 to 31 March 2026 | 31 December 2026 |

The most significant upcoming deadline is 30 September 2026, which applies to businesses with a financial year ending 31 December 2025. This is the deadline for the majority of UAE businesses operating on a calendar-year financial year.

Payment Must Arrive, Not Just Be Initiated

The FTA treats the payment deadline as the date funds are received by the authority, not the date the transfer is initiated. Businesses paying via international bank transfer should account for processing time and initiate payment several working days before the deadline.

6. Corporate Tax for Free Zone Companies

Free zone companies operating in the UAE are subject to corporate tax under the same Decree-Law as mainland businesses. However, the law preserves the UAE’s historical free zone tax incentives through the concept of the Qualifying Free Zone Person (QFZP).

Qualifying Free Zone Person (QFZP)

A free zone entity that meets all the conditions of a QFZP under Article 18 of Federal Decree-Law No. 47 of 2022, Cabinet Decision No. 100 of 2023, and Ministerial Decision No. 265 of 2023 pays:

- 0% on qualifying income

- 9% on taxable income that is not qualifying income, with no AED 375,000 threshold available

To maintain QFZP status in a tax period, a free zone entity must satisfy all five conditions simultaneously:

- Adequate substance in the free zone: The entity must maintain sufficient assets, qualified employees, and operating expenditure in the free zone for the activities that generate qualifying income.

- Derive qualifying income: As defined in Cabinet Decision No. 100 of 2023, qualifying income includes income from transactions with other free zone persons, income from qualifying activities carried out in or from a free zone or designated zone, and income from certain other sources specified in the Ministerial Decision.

- No election for standard rates: The entity must not have made an irrevocable election to be subject to UAE corporate tax at the standard 9% rate. Once made, this election cannot be reversed.

- Comply with transfer pricing rules: All transactions with related parties must be conducted at arm’s length.

- Audited financial statements: QFZPs are required to prepare audited financial statements. This is not optional even where a company would otherwise fall below auditing thresholds.

De Minimis Rule

A free zone entity does not lose QFZP status if non-qualifying income does not exceed the lower of AED 5 million or 5% of total revenue in the tax period (the de minimis threshold under Cabinet Decision No. 100 of 2023). Income within the de minimis limit is still taxed at 9%.

What Counts as Qualifying Income

Qualifying income for QFZP purposes includes income from:

- Transactions with other free zone persons, unless the income relates to an excluded activity

- Qualifying activities carried out with non-free zone persons, as specified in Cabinet Decision No. 100 of 2023 (including manufacturing, processing, logistics, fund management, wealth and investment management, headquarter services to related parties, treasury and financing services to related parties, aircraft financing and leasing, and distribution of goods in or from designated zones)

- Income from intellectual property assets meeting the conditions of Ministerial Decision No. 229 of 2025

Income from excluded activities, including banking and insurance services provided to non-free zone persons and income from immovable property outside designated zones, does not qualify.

Filing Obligation Applies Regardless of Rate All free zone entities, including those with full QFZP status and zero taxable income, must file an annual corporate tax return. Failure to file can result in loss of QFZP status for that tax period.

7. Small Business Relief in UAE

Small Business Relief in UAE (SBR) is a transitional measure introduced under Article 21 of Federal Decree-Law No. 47 of 2022 and Ministerial Decision No. 73 of 2023. It allows eligible businesses to elect to be treated as having zero taxable income, effectively paying no corporate tax.

Eligibility Conditions

A resident person may elect for Small Business Relief in a tax period if:

- Revenue for that tax period does not exceed AED 3 million

- The election is made on the corporate tax return for that period

- The tax period ends on or before 31 December 2026

Revenue for this purpose means the gross amount of income derived during the tax period before deducting any expenses.

Who Cannot Elect Small Business Relief

- Businesses that are part of a multinational enterprise group with consolidated global revenue exceeding EUR 750 million

- Qualifying Free Zone Persons

- Entities that are members of a Tax Group

Effect of Electing SBR

When a business elects Small Business Relief, it is treated as having no taxable income for that period, which means no corporate tax liability arises. However, the business is still required to register for UAE corporate tax and file a return declaring the election. Transfer pricing documentation requirements and certain other obligations are simplified but not entirely removed.

SBR Must Be Actively Elected Small Business Relief does not apply automatically. The election must be made each tax period on the corporate tax return filed via EmaraTax. A business that meets the revenue threshold but forgets to elect SBR will be assessed on its actual taxable income.

SBR is a Transitional Measure

SBR is only available for tax periods ending on or before 31 December 2026. Businesses planning their tax position for periods ending after this date should not rely on SBR and should review their corporate tax exposure accordingly.

GET STARTED TODAY

Let mazeed Handle Your Corporate Tax

Join 4,000+ UAE businesses using mazeed to stay compliant and avoid costly mistakes.

8. How Taxable Income is Calculated

Taxable income is calculated starting from the accounting net profit or loss as reported in the financial statements, which must be prepared in accordance with International Financial Reporting Standards (IFRS) or IFRS for SMEs.

From this starting point, a number of adjustments are required under the Decree-Law and Ministerial Decision No. 134 of 2023 on the General Rules for Determining Taxable Income:

- Add back non-deductible expenses (fines, penalties, personal expenses, excess interest, amounts paid to related parties above arm’s length)

- Deduct exempt income (dividends from participating interests, gains on disposal of participating interests meeting the Participation Exemption conditions)

- Apply any elected reliefs (Small Business Relief, Tax Group consolidation)

- Offset available tax losses carried forward from prior periods (subject to a 75% limit per period under Article 39)

The result is taxable income, to which the applicable rate (0% or 9%) is applied.

9. Allowable Deductions

Business expenses are generally deductible if they are incurred wholly and exclusively for the purposes of the taxable person’s business and are not specifically excluded under the Decree-Law. Key categories of deductible expenditure include:

Deductible Expenses

- Staff costs: Salaries, wages, bonuses, employer pension contributions, end-of-service gratuity accruals under UAE Labour Law, and staff housing allowances are fully deductible if at arm’s length and documented.

- Depreciation and amortisation: Tax depreciation follows IFRS depreciation except for capitalised interest, which is subject to the interest deduction rules. Ministerial Decision No. 173 of 2025 introduced an irrevocable election for deemed depreciation on investment properties carried at fair value.

- Rent and occupancy costs: Deductible where incurred for business purposes and documented.

- Professional fees: Accounting, audit, legal, and advisory fees incurred for business purposes.

- Marketing and advertising: Generally deductible if for business purposes.

- Entertainment: 100% deductible for employee-related entertainment; 50% deductible for client and supplier entertainment.

Interest Deduction Limitation

Under Ministerial Decision No. 126 of 2023 on the General Interest Deduction Limitation Rule, net interest expenditure (interest expense minus interest income) is deductible up to the higher of:

- AED 12 million per tax period (the safe harbour), or

- 30% of tax-adjusted EBITDA for the period

Net interest expenditure above this limit is non-deductible in the current period but may be carried forward for up to 10 subsequent tax periods. Interest on loans obtained from related parties for specific transactions such as dividend payments or return of capital carries an additional specific limitation rule.

Non-Deductible Corporate Tax Items

- Administrative fines and penalties imposed by government authorities

- Dividends and profit distributions to shareholders

- Personal expenses of owners or shareholders

- Bribes or payments that are illegal under UAE law

- Expenses paid to related parties above an arm’s length amount

Transfer Pricing

All transactions between related parties must be priced at arm’s length under Article 34 of the Decree-Law. Under Ministerial Decision No. 97 of 2023, businesses with revenue exceeding AED 200 million must maintain a Master File and Local File for transfer pricing documentation. Multinational enterprise groups with global revenue exceeding EUR 750 million are also subject to country-by-country reporting requirements.

10. How to File Your UAE Corporate Tax Return

All corporate tax returns must be submitted electronically through the EmaraTax portal at eservices.tax.gov.ae. Returns cannot be filed by paper or email.

Documents to Prepare Before Filing

- Audited or finalised financial statements (income statement, balance sheet, cash flow statement) for the relevant tax period

- Corporate Tax Registration Certificate (TRN)

- Trade licence

- Supporting documents for all deductions claimed

- Transfer pricing disclosure form (if applicable)

- Evidence of any exemptions elected (SBR election, QFZP status confirmation)

UAE Corporate Tax Filing Steps

1- Finalise financial statements

Prepare IFRS-compliant financial statements for the tax period. If your business is required to have audited accounts, the audit should be completed before filing. Free zone QFZPs must have audited accounts regardless of size.

2- Calculate taxable income

Start from accounting profit and make all required adjustments for non-deductible items, exempt income, and applicable reliefs. Document the basis for each adjustment.

3- Log in to EmaraTax

Access the portal at eservices.tax.gov.ae using UAE Pass and navigate to the corporate tax return for the relevant tax period.

4- Complete all sections of the return

The return requires disclosure of: revenue, taxable income, tax liability, elections made (SBR, QFZP), related party transactions, and details of any tax losses carried forward.

5- Submit the return and pay

Submit the completed return and pay any tax liability due. Both must be completed by the same deadline. The FTA’s EmaraTax portal supports payment via UAE bank transfer using a GIBAN (Generated International Bank Account Number) assigned to each taxpayer. International transfers are accepted but carry a risk of processing delays.

Do Not Leave Filing to the Last Day The FTA has publicly warned businesses against waiting until the deadline, noting that system load increases significantly in the days before major deadlines and that bank transfers may not be processed in time. The FTA guidance is to file and pay at least a week before the deadline where possible.

Source: Federal Tax Authority Press Release, 24 September 2025. tax.gov.ae

11. Penalties for Non-Compliance

The FTA administers a structured penalty regime for UAE corporate tax non-compliance. Key penalties include:

| Violation | Penalty |

| Failure to register for corporate tax by the prescribed deadline | AED 10,000 |

| Failure to file a corporate tax return by the deadline | AED 500 per month for the first 12 months; AED 1,000 per month thereafter |

| Failure to pay corporate tax by the deadline | 2% of unpaid tax immediately; 4% per month from one month after the deadline |

| Failure to maintain required records | AED 10,000 for first instance; AED 50,000 for repeat violations |

| Failure to submit a transfer pricing disclosure form | AED 1,000 per month up to a maximum of AED 250,000 |

Corporate Tax Penalty Waiver

The FTA has offered a temporary waiver on the AED 10,000 late registration penalty for businesses that file their first corporate tax return or annual declaration within seven months of the end of their first tax period. Businesses that have not yet registered should seek urgent professional advice on whether this waiver still applies to their situation.

Read more: UAE Corporate Tax Penalties

12. Natural Persons and Sole Proprietors

UAE corporate tax applies to natural persons who conduct business activities in the UAE and whose total business income exceeds AED 1 million in a Gregorian calendar year. This threshold applies to the individual’s total business revenue from all sources, not to profit.

Natural persons subject to corporate tax include freelancers, sole proprietors, and self-employed professionals operating under individual trade licences or professional licences. Employment income, investment income (where not part of a business activity), and personal income from real property owned in a personal capacity are not subject to corporate tax.

A natural person who meets the AED 1 million threshold must:

- Register for corporate tax by 31 March of the following Gregorian calendar year

- File a corporate tax return for each tax year in which they exceed the threshold

- Maintain records of all business income and expenditure

Natural Persons and Small Business Relief

Natural persons who exceed the AED 1 million registration threshold but have revenue of AED 3 million or below may elect Small Business Relief, effectively reducing their corporate tax liability to zero for eligible periods.

13. Frequently Asked Questions about UAE Corporate Tax

What is the UAE corporate tax rate?

The corporate tax rate under Federal Decree-Law No. 47 of 2022 is 0% on taxable income up to AED 375,000 and 9% on taxable income above AED 375,000. Qualifying Free Zone Persons pay 0% on qualifying income and 9% on non-qualifying income.

When is the UAE corporate tax filing deadline for businesses with a December year end?

For businesses with a financial year ending 31 December 2025, the corporate tax return and payment are both due by 30 September 2026. Both must be completed by this date; filing without paying or paying without filing are both treated as non-compliance by the FTA.

Do I need to file a UAE corporate tax return if I owe no tax?

Yes. Filing is mandatory for all registered taxable persons regardless of whether any tax is owed. This includes businesses within the 0% income band, businesses electing Small Business Relief, and free zone companies with full QFZP status. The FTA confirmed this in its September 2025 compliance reminder.

Can I file a corporate tax return without audited accounts?

Businesses that are not legally required to have audited accounts may file based on management accounts prepared under IFRS or IFRS for SMEs. However, Qualifying Free Zone Persons must have audited financial statements. Companies should check their free zone authority’s requirements independently, as some free zones mandate audits for all entities regardless of size.

What happens if I miss the UAE corporate tax filing deadline?

A penalty of AED 500 per month applies for the first 12 months of late filing, rising to AED 1,000 per month thereafter. Late payment penalties of 2% of the unpaid tax apply immediately, followed by 4% per month from one month after the deadline. There is no provision for a general extension to the filing deadline.

Does UAE corporate tax apply in all seven emirates?

Yes. Corporate tax under Federal Decree-Law No. 47 of 2022 is a federal tax that applies across all seven emirates of the UAE. Businesses in Abu Dhabi, Sharjah, Ajman, Umm Al Quwain, Ras Al Khaimah, and Fujairah are subject to the same rules as businesses in Dubai.

Is my holding company subject to UAE corporate tax?

Yes, if it is a UAE resident juridical person. However, holding companies may benefit from the Participation Exemption under Article 23 of the Decree-Law, which exempts dividends and capital gains from qualifying shareholdings from corporate tax, subject to conditions. Specialist advice is recommended for holding structures.

Official References and Sources

- Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses. Ministry of Finance.

- Federal Tax Authority Corporate Tax Legislation Page. Includes all Cabinet Decisions and Ministerial Decisions.

- Ministerial Decision No. 73 of 2023 on Small Business Relief for the Purposes of Federal Decree-Law No. 47 of 2022. Ministry of Finance.

- Cabinet Decision No. 100 of 2023 on Determining Qualifying Income of a Qualifying Free Zone Person. Cabinet of the UAE.

- Ministerial Decision No. 265 of 2023 on Qualifying Activities and Excluded Activities. Ministry of Finance.

- Ministerial Decision No. 126 of 2023 on the General Interest Deduction Limitation Rule. Ministry of Finance.

- Ministerial Decision No. 97 of 2023 on Transfer Pricing Documentation Requirements. Ministry of Finance.

- Ministerial Decision No. 134 of 2023 on General Rules for Determining Taxable Income. Ministry of Finance.

- FTA Decision No. 3 of 2024 on Timelines for Corporate Tax Registration. Federal Tax Authority.

- Federal Tax Authority Press Release: “FTA Urges Submission of Corporate Tax Returns Within Nine Months.” 24 September 2025.

- FTA Corporate Tax Guide: Free Zone Persons (CTGFZP1). May 2024. Federal Tax Authority.

- FTA Corporate Tax Guide: Determination of Taxable Income (CTGDTI1). Federal Tax Authority.

- Ministerial Decision No. 173 of 2025 on Depreciation Adjustments for Investment Properties. Ministry of Finance.

- Ministerial Decision No. 229 of 2025 on Qualifying Income from Intellectual Property. Ministry of Finance.

Disclaimer: This publication is for informational purposes only and should not be considered professional or legal advice. While we strive for accuracy, we make no guarantees regarding completeness or applicability. mazeed, its members, employees, and agents do not accept or assume any liability, responsibility, or duty of care for any actions taken or decisions made based on this content. For official tax guidance, please refer to the UAE Ministry of Finance and the Federal Tax Authority.