Small Business Relief is the most significant Corporate Tax concession available to UAE businesses right now, and it expires on 31 December 2026. Established under Article 21 of Federal Decree-Law No. 47 of 2022 and governed by Ministerial Decision No. 73 of 2023, it allows eligible resident businesses with revenue at or below AED 3 million to elect to pay zero Corporate Tax for any qualifying tax period. This guide covers every eligibility condition, who is excluded, the election process on EmaraTax, the trade-off with tax loss carry-forward, and how to prepare for the end of the relief period.

🡆 This article covers Small Business Relief in full detail. For a complete overview of UAE corporate tax including rates, registration, filing deadlines, free zone rules, and deductions, read the UAE Corporate Tax 2026: Complete Guide for Businesses.

1. What Is Small Business Relief in UAE

Small Business Relief (SBR) is a transitional tax measure introduced by the UAE Ministry of Finance to reduce the Corporate Tax burden and compliance costs for small businesses and startups during the initial years of the UAE Corporate Tax regime. Under Small business relief in UAE, an eligible resident taxable person is treated as having zero taxable income for the relevant tax period, meaning no Corporate Tax liability arises regardless of actual profit.

The relief was designed with two purposes. First, to provide a practical cushion for small enterprises entering the UAE Corporate Tax system for the first time. Second, to reduce the administrative load on micro and small businesses that would otherwise be required to prepare full taxable income calculations under standard Corporate Tax rules.

The Ministry of Finance described the intent in its official announcement of Ministerial Decision No. 73 of 2023: the relief is intended to support startups and other small or micro businesses by reducing their Corporate Tax burden and compliance costs. The Deloitte assessment of the decision confirmed it as a significant and broadly positive development for the UAE SME sector.

Transitional Measure with a Firm End Date

small business relief in UAE is available only for tax periods ending on or before 31 December 2026. The Ministry of Finance has not announced any extension. Businesses should treat this date as firm when planning their tax position for 2027 and beyond.

Quick Eligibility Check for Small Business Relief in UAE

2. Legal Basis and Official Source

small business relief in UAE is established in the following official instruments:

- Article 21 of Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses: the primary legal authority for Small Business Relief, which empowers the Minister of Finance to prescribe the revenue threshold and conditions.

- Ministerial Decision No. 73 of 2023 on Small Business Relief for the Purposes of Federal Decree-Law No. 47 of 2022: sets the AED 3 million revenue threshold, eligibility conditions, treatment of tax losses, disallowed interest, and the anti-avoidance rule for artificial business separation.

- FTA Corporate Tax Guide CTGSBR1 (Small Business Relief, August 2023): the FTA’s official interpretive guidance on the operation of SBR, including worked examples. Published on the FTA website at tax.gov.ae.

- Article 50 of Federal Decree-Law No. 47 of 2022: the General Anti-Abuse Rule, which applies where the FTA determines that a business has artificially separated its activities to qualify for SBR.

All conditions and thresholds described in this guide are drawn from these primary sources.

GET STARTED TODAY

Let mazeed Handle Your Corporate Tax

Join 4,000+ UAE businesses using mazeed to stay compliant and avoid costly mistakes.

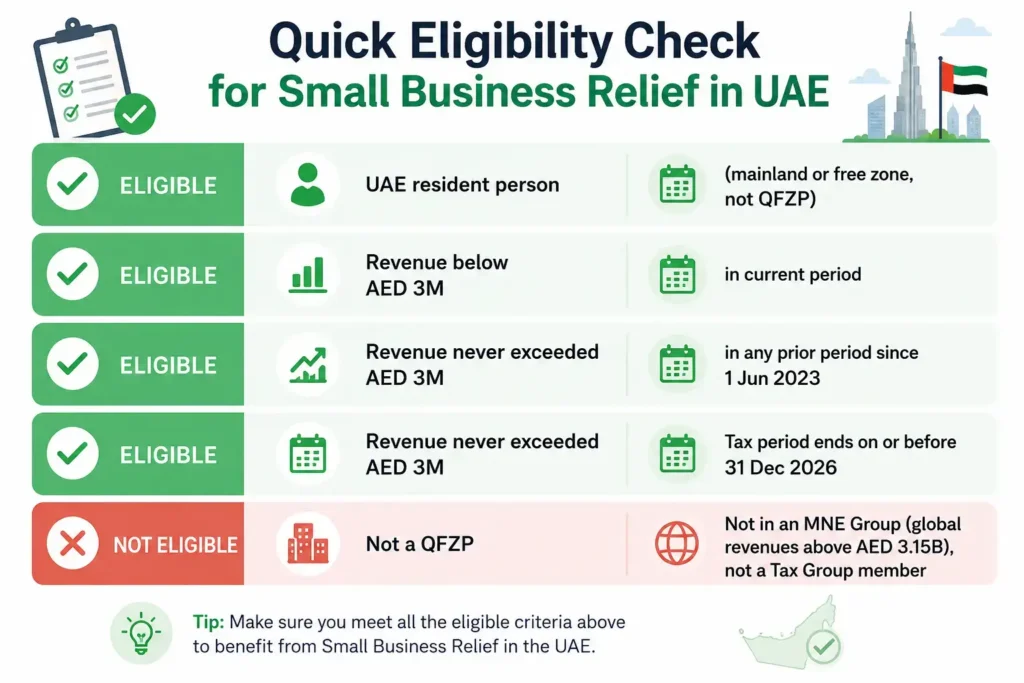

3. Eligibility Conditions for Small Business Relief in UAE

To qualify for Small Business Relief in UAE, a taxable person must satisfy all of the following conditions simultaneously in the relevant tax period:

Condition 1: Must Be a Resident Person

Only resident taxable persons are eligible for SBR. Under Article 11 of Federal Decree-Law No. 47 of 2022, a resident person includes a juridical person incorporated or recognised under UAE law (including free zone entities that are not QFZPs), and a natural person conducting business in the UAE.

Non-resident persons, whether juridical or natural, are not eligible for Small Business Relief in UAE regardless of the level of UAE-sourced income.

Condition 2: Revenue Must Not Exceed AED 3 Million in the Current Period

Revenue for the relevant tax period must be at or below AED 3 million. Revenue is calculated based on applicable accounting standards accepted in the UAE, meaning IFRS or IFRS for SMEs. Revenue excludes VAT collected on behalf of the government. It includes all income from business activities, regardless of source, including income from foreign operations of a UAE-resident entity.

Condition 3: Revenue Must Not Have Exceeded AED 3 Million in Any Prior Period

This is the condition most commonly overlooked. Under Ministerial Decision No. 73 of 2023, Small Business Relief is not available in a tax period if the taxable person’s revenue exceeded AED 3 million in any previous tax period since 1 June 2023. The Ministry of Finance’s official announcement stated this explicitly: once a taxable person exceeds the AED 3 million threshold in any tax period, Small Business Relief in UAE will no longer be available in any subsequent period.

This means the AED 3 million limit functions as a permanent disqualifier, not a year-by-year test. A business that earned AED 3.1 million in 2023, then AED 2.5 million in 2024, is not eligible for SBR in 2024 because it exceeded the threshold in the prior period.

Condition 4: The Tax Period Must End on or Before 31 December 2026

SBR is only available for tax periods ending on or before 31 December 2026. The relief applies to financial years commencing on or after 1 June 2023. A business with a financial year ending 31 December 2026 can claim SBR for that year if it meets all other conditions. A business with a financial year ending 31 March 2027 cannot claim SBR for that period even if it meets the revenue threshold.

The Prior Period Rule Is Permanent

A business that exceeded AED 3 million in revenue in any tax period since 1 June 2023 is permanently excluded from Small Business Relief in UAE in all future periods, including periods where revenue subsequently falls below the threshold. There is no mechanism to re-enter the SBR regime once the threshold has been crossed.

4. Who Is Excluded from Small Business Relief in UAE

Even where the AED 3 million revenue threshold is met, the following categories of person cannot claim Small Business Relief in UAE:

- Qualifying Free Zone Persons (QFZPs). Free zone entities that have elected or qualify for the 0% rate on qualifying income under Article 18 of the Decree-Law are expressly excluded from SBR. A QFZP benefits from the 0% qualifying income rate through a separate mechanism and cannot additionally claim SBR.

- Constituent companies of Multinational Enterprise Groups (MNE Groups). A business that forms part of a group with consolidated global revenues exceeding AED 3.15 billion (approximately EUR 750 million) under Cabinet Decision No. 44 of 2020 cannot claim Small Business Relief, regardless of the individual entity’s UAE revenue. This exclusion aligns with OECD Pillar Two standards.

- Members of a Tax Group. Businesses that have elected to form a Tax Group under Article 40 of the Decree-Law are assessed on a consolidated basis and cannot separately elect Small Business Relief at the individual entity level during the group period.

- Non-resident persons. As noted above, only resident persons are eligible. Non-residents with UAE permanent establishments or nexus are assessed under different rules.

Free Zone Companies That Are Not QFZPs

A free zone company that has not elected QFZP status, or whose income does not meet the qualifying income conditions, is subject to standard Corporate Tax rates. Such a company is a resident person for Corporate Tax purposes and may be eligible for Small Business Relief in UAE if it meets the AED 3 million revenue threshold and all other conditions.

5. How Revenue Is Calculated for Small Business Relief Purposes

Revenue for Small Business Relief eligibility purposes is determined in accordance with the applicable accounting standards accepted in the UAE. For most UAE businesses, this means IFRS or IFRS for SMEs. The FTA’s Corporate Tax Guide CTGSBR1 confirms that revenue is not a reference to taxable income or net profit: it is gross revenue before deducting any expenses.

What Is Included in Revenue

- All income from the sale of goods and provision of services

- Rental income where forming part of business activities

- Interest income where forming part of business activities

- Income from royalties, licences, and intellectual property where part of business activities

- All other income recognised as revenue under applicable accounting standards

What Is Excluded from Revenue

- VAT collected on behalf of the government: revenue is calculated excluding VAT

- Capital gains on the disposal of assets are generally excluded from revenue for accounting purposes, though this depends on the nature of the business and applicable accounting treatment

- Dividends received from subsidiaries, where not forming part of ordinary business activities under applicable accounting standards

Using Cash Basis Accounting

The FTA has confirmed in its official guidance that eligible SBR-electing businesses may use cash basis accounting for simplicity, provided this is consistent with their circumstances and size. However, revenue tracking must be accurate and supported by invoices, bank statements, and financial records. The FTA can and does audit SBR claims retrospectively, cross-referencing declared revenue against VAT returns and bank data.

Revenue Includes All Business Streams

For natural persons conducting multiple business activities, all revenue from all business streams is aggregated when assessing the AED 3 million threshold. A freelancer who earns AED 1.5 million from consultancy and AED 1.8 million from property management as a business has combined business revenue of AED 3.3 million and does not qualify for Small Business Relief for that period.

6. What Small Business Relief Actually Does

When a business validly elects Small Business Relief in UAE for a tax period, the following consequences apply under Article 21 of the Decree-Law and Ministerial Decision No. 73 of 2023:

- Zero taxable income: The business is treated as having no taxable income for that tax period. The actual accounting profit is irrelevant. A business with AED 500,000 in profit pays no Corporate Tax in an SBR period.

- Zero Corporate Tax liability: No Corporate Tax is calculated, assessed, or paid for the period in which SBR is elected.

- No requirement to calculate taxable income: The complex adjustments required under the standard regime, including adding back non-deductible expenses and applying exemptions, are not required for an SBR period.

- Simplified tax return: SBR electors file a simplified Corporate Tax return on EmaraTax. The return confirms the election, declares total revenue, and records the SBR election. The full taxable income computation required of non-SBR filers is not needed.

- No transfer pricing documentation: SBR electors are not required to maintain the transfer pricing documentation otherwise required under Ministerial Decision No. 97 of 2023 for qualifying periods. Standard arm’s length principles still apply but documentation requirements are simplified.

What SBR Does Not Exempt You From

Small Business Relief does not exempt a business from Corporate Tax registration, annual return filing, or record-keeping obligations. All SBR-electing businesses must be registered with the FTA, file a return each year, and maintain revenue records for at least seven years from the end of the relevant tax period to substantiate eligibility.

Software & Experts Together!

New Way to Manage Corporate Tax in UAE

Just scan your invoices and our team will handle all your compliance process inside your mazeed account.

7. Simplified Compliance Under Small Business Relief in UAE

One of the stated objectives of the SBR regime is to reduce administrative complexity for small businesses. The FTA’s Corporate Tax Guide CTGSBR1 sets out the specific compliance simplifications available to SBR electors:

| Compliance Requirement | Standard Regime | SBR Regime |

| Taxable income calculation | Full calculation required with all adjustments | Not required. Treated as zero. |

| Transfer pricing documentation | Required for businesses above AED 200M revenue threshold | Not required. Arm’s length standard still applies. |

| Corporate Tax return | Full return with all schedules | Simplified return. Revenue declared, election made. |

| Tax loss carry-forward calculation | Losses calculated and declared for future use | Not permitted. Losses forfeited for SBR periods. |

| Net interest expenditure carry-forward | Excess calculated and carried forward up to 10 years | Not permitted. Disallowed interest forfeited for SBR periods. |

| Corporate Tax registration | Mandatory for all taxable persons | Mandatory. SBR does not exempt from registration. |

| Annual return filing | Required within 9 months of financial year end | Required. Simplified form but same deadline. |

| Revenue record retention | 7 years minimum | 7 years minimum. FTA audits SBR claims retrospectively. |

8. The Trade-Off: When Not to Elect Small Business Relief in UAE

Small Business Relief is not always the right choice for every eligible business. The key trade-off is the permanent forfeiture of tax losses and disallowed net interest expenditure for any period in which SBR is elected. This has material long-term implications for businesses that are currently loss-making or that carry significant debt.

Ministerial Decision No. 73 of 2023 is explicit: electing for SBR in a tax period means any tax losses incurred in that period cannot be declared to the FTA and cannot be carried forward for use in future periods. Similarly, any disallowed net interest expenditure from an SBR period is permanently forfeited.

Elect SBR: Suitable When

- The business is profitable and paying zero tax immediately has clear cash benefit

- Revenue is well below AED 3 million with no near-term growth plan that would push above the threshold

- The business carries no significant accumulated tax losses or excess interest

- Reducing compliance burden is a priority

- The business is in its first one or two years of operation with minimal losses

Do Not Elect SBR: Consider Standard Regime When

- The business is loss-making and those losses would reduce taxable income in future profitable years

- Significant net interest expenditure is being incurred that could be carried forward under the standard regime

- The business is growing rapidly and expects revenue to exceed AED 3 million within one to two years

- Future periods are expected to be significantly more profitable, and current losses could offset that future liability

- The business is in a capital-intensive early phase with large upfront losses

How to Run the Calculation

Before electing SBR, calculate the value of any tax losses that would be forfeited. Apply the 9% rate to those losses and compare it to the zero-tax benefit of SBR in the current period. If the future tax shield from carrying forward losses is worth more than the immediate tax saving, the standard regime is likely the better choice. A qualified UAE tax advisor can model this for your specific numbers.

Example: Loss-Making Business. Should It Elect SBR?

Situation: A Dubai LLC in its second year of operation has revenue of AED 2.4 million and a net loss of AED 800,000 for the year ending 31 December 2025. It meets all SBR eligibility conditions.

If SBR is elected: The business pays zero Corporate Tax for 2025. The AED 800,000 loss cannot be carried forward. In 2026, if the business becomes profitable with taxable income of AED 600,000, the full 9% rate applies to AED 600,000 above AED 375,000, resulting in a tax liability of AED 20,250.

If SBR is not elected: The business pays zero Corporate Tax for 2025 anyway (because the loss means there is no taxable income and the 0% threshold absorbs the first AED 375,000). The AED 800,000 loss is declared and carried forward. In 2026, with taxable income of AED 600,000, up to 75% of that income (AED 450,000) can be offset by the carried-forward loss, reducing taxable income substantially. Tax liability for 2026 is significantly reduced.

Conclusion: For a loss-making business, the standard regime is almost always the better choice. The SBR election provides no immediate benefit (there is nothing to pay) while permanently eliminating a valuable future tax asset.

9. How to Elect Small Business Relief on EmaraTax

The SBR election is made on the Corporate Tax return filed through EmaraTax. It is not a separate application or pre-filing step. The election must be made each year for each tax period in which SBR is desired. Failing to make the election in a year means the standard Corporate Tax rules apply for that year, even if the business was otherwise eligible.

- Confirm eligibility before filing

- Before logging in to EmaraTax, verify that revenue in the current period did not exceed AED 3 million and that revenue in all prior periods since 1 June 2023 also did not exceed AED 3 million. Confirm the entity is not a QFZP and is not part of an MNE Group. Compile the revenue records that will support the election.

- Log in to EmaraTax and open the Corporate Tax return

- Access the portal at eservices.tax.gov.ae using UAE Pass. Navigate to the Corporate Tax module and open the tax return for the relevant tax period.

- Complete the entity details and revenue declaration

- Enter the required entity information and declare total revenue for the tax period. This figure is the basis for the FTA’s assessment of SBR eligibility. Use the figure derived from IFRS or IFRS for SMEs financial records, excluding VAT.

- Navigate to the Elections section and select Small Business Relief

- Within the return, locate the Elections section. This is a dedicated part of the return form where various Corporate Tax elections are made. Explicitly select the Small Business Relief election for the current tax period. The system will confirm the election has been recorded. This step is not pre-selected and is easy to miss.

- Complete the simplified return and submit

- Once SBR is elected, the return shifts to a simplified format. Taxable income calculation fields are removed or pre-populated as zero. Review the simplified summary, confirm the accuracy declaration, and submit. EmaraTax issues immediate confirmation of the election upon submission. Download and retain the confirmation as part of your tax records.

The Election Cannot Be Revoked After Submission

Once the SBR election is made and the return is submitted on EmaraTax, the election cannot be revoked for that tax period. If the election is made in error or the business subsequently determines it was not eligible, a voluntary disclosure may be available in limited circumstances, but this is subject to FTA assessment and may carry penalties. The election decision should be made carefully before filing.

10. After December 2026: What Comes Next

small business relief in UAE is available only for tax periods ending on or before 31 December 2026. For a business with a financial year ending 31 December 2026, this is the last year in which SBR can be elected. For a business with a financial year ending 31 March 2026, the tax period ending 31 March 2026 is within the SBR window, but the next period ending 31 March 2027 falls outside it.

From the first tax period ending after 31 December 2026, all businesses regardless of size will be subject to the standard UAE Corporate Tax rates:

- 0% on taxable income up to AED 375,000

- 9% on taxable income above AED 375,000

This means businesses that relied on SBR and have revenue consistently below AED 3 million will still pay zero Corporate Tax in most cases under the standard regime, because their taxable income is unlikely to exceed AED 375,000. However, they will need to:

- Prepare full taxable income calculations and a complete tax return

- Maintain transfer pricing documentation if applicable

- Track and carry forward any tax losses and disallowed interest under standard rules

- Comply with all standard record-keeping and audit requirements

Preparing for the Post-2026 Period

Businesses currently relying on SBR should use 2026 to establish proper accounting systems, move to IFRS-compliant bookkeeping if not already doing so, and understand their likely taxable income position from 2027 onwards. The administrative step-up is meaningful, and preparation during the SBR period reduces the risk of compliance gaps in the first post-SBR year.

11. Anti-Avoidance: Artificial Business Separation

Ministerial Decision No. 73 of 2023 includes a specific anti-avoidance provision targeted at businesses that attempt to circumvent the AED 3 million threshold by artificially splitting a single business across multiple entities, each of which individually remains below the threshold.

Where the FTA determines that taxable persons have artificially separated their business or business activity, and the total revenue of the entire business or business activity exceeds AED 3 million in any tax period, this constitutes a Corporate Tax advantage under Article 50 of the Decree-Law (the General Anti-Abuse Rule). The FTA can aggregate the revenue of all related entities and disqualify all of them from SBR for the relevant period.

The FTA’s enforcement note published in 2026 confirmed that its risk-based audit programme specifically targets SBR claimants. Common audit triggers include:

- Revenue declarations that fall to just below AED 3 million after periods above that level

- Multiple related entities each claiming SBR, with combined revenue that significantly exceeds AED 3 million

- Revenue declared for Corporate Tax purposes that is inconsistent with VAT return figures for the same period

- Transactions between related SBR-electing entities that appear designed to shift revenue between periods or entities

Penalties for Artificial Separation

Where the FTA determines that artificial separation has occurred, consequences include full recovery of Corporate Tax on the aggregated revenue of all entities, a 15% administrative penalty on recovered tax, potential retrospective disqualification from SBR for prior periods already assessed, and reputational risk from FTA audit proceedings. Legitimate business restructuring is not affected, but any structure whose primary purpose is to keep entities below the SBR threshold carries significant risk.

12. Worked Examples

Example 1: Straightforward SBR Election

Scenario: Profitable Mainland LLC, Calendar Year

Facts: A Dubai mainland LLC operates a management consultancy. Revenue for the year ending 31 December 2025 is AED 2.2 million. Revenue for the first tax period (2024) was AED 1.8 million. Net profit is AED 650,000. The company has no accumulated tax losses and no significant debt.

Eligibility: The company is a UAE resident juridical person. Revenue is below AED 3 million in 2025 and in the prior period (2024). It is not a QFZP or part of an MNE Group.

If SBR is elected: The company is treated as having zero taxable income. No Corporate Tax is payable. Filing a simplified return on EmaraTax is all that is required. Without SBR, the company would pay 9% on AED 275,000 (the amount above AED 375,000), equalling AED 24,750.

Conclusion: SBR is clearly the right choice. There are no losses to preserve, the saving is AED 24,750 in cash, and compliance is simplified.

Example 2: Natural Person Approaching the Threshold

Scenario: Abu Dhabi Freelancer, Tax Year 2025

Facts: A self-employed architect operating under a personal trade licence in Abu Dhabi has business revenue of AED 2.9 million in the year ending 31 December 2025. This is the first year revenue has exceeded AED 1 million, making this his first taxable period. Net income after expenses is AED 900,000.

Eligibility: He is a UAE resident natural person conducting business. Revenue is below AED 3 million. He has no prior tax periods above the threshold. He is not a QFZP or MNE constituent. He is eligible for SBR.

Consideration: If he expects 2026 revenue to exceed AED 3 million due to new projects, he should note that 2025 is likely his last year to claim SBR regardless, as the 2025 revenue of AED 2.9 million is close to the threshold and 2026 may push him over permanently. He may wish to elect SBR in 2025 and prepare for standard filing in 2026.

Conclusion: Elect SBR for 2025. The saving is meaningful (9% on AED 525,000 above AED 375,000, equalling AED 47,250). Use 2025 to establish proper accounting systems for the post-SBR period.

Example 3: Previously Exceeded Threshold

Scenario: Sharjah Trading Company, Revenue Declined

Facts: A Sharjah trading company had revenue of AED 4.2 million in its first tax period (year ending 31 December 2024). In 2025, revenue declined to AED 2.7 million due to a lost contract.

Eligibility: The company is not eligible for Small Business Relief in UAE in 2025. Although 2025 revenue is below AED 3 million, the company exceeded the threshold in a prior tax period (2024). Under Ministerial Decision No. 73 of 2023, this permanently disqualifies the company from SBR for all subsequent periods.

What to do: File a standard Corporate Tax return for 2025. Calculate taxable income on the standard basis. Apply the 0% rate to the first AED 375,000 and 9% to any taxable income above that. Carry forward any tax losses or disallowed interest from prior periods under the standard rules.

13. Frequently Asked Questions about Small Business Relief in UAE

Who qualifies for Small Business Relief in UAE?

A UAE resident taxable person qualifies if their revenue did not exceed AED 3 million in the relevant tax period and in all previous tax periods since 1 June 2023. They must not be a Qualifying Free Zone Person, a constituent company of an MNE Group with global revenues above AED 3.15 billion, or a Tax Group member.

Is Small Business Relief in UAE automatic?

No. The election must be made actively in the Elections section of the Corporate Tax return filed on EmaraTax for each tax period. Failure to make the election means the standard Corporate Tax regime applies, even where the business meets all eligibility conditions.

Can a free zone company claim Small Business Relief?

A free zone company that is not a Qualifying Free Zone Person may be eligible for Small Business Relief if it meets the AED 3 million revenue threshold and all other conditions. A Qualifying Free Zone Person cannot claim Small Business Relief. The position of each free zone entity depends on whether it has elected QFZP status and whether that status is maintained.

What happens if I elect SBR but my revenue actually exceeded AED 3 million?

Claiming SBR when the revenue threshold has been exceeded is a compliance failure. The FTA can audit, recover the unpaid Corporate Tax, and impose administrative penalties. Maintaining accurate revenue records and reviewing them before making the election is essential. If an error is discovered after filing, a voluntary disclosure through EmaraTax may be possible but will carry penalties for any tax shortfall.

Can I claim Small Business Relief for some years and not others?

Yes, provided eligibility conditions are met each year, including the prior period revenue condition. A business may elect SBR in 2024, choose not to elect it in 2025 (for example, to preserve tax losses), and elect again in 2026, if it remains below the AED 3 million threshold in all periods and meets all other conditions.

Do I still need to file a Corporate Tax return if I claim Small Business Relief in UAE?

Yes. Registered taxable persons must file an annual return regardless of whether SBR is elected. The return filed by SBR electors is a simplified version and does not require a full taxable income calculation, but the filing deadline (nine months from financial year end) applies equally.

What records do I need to keep for Small Business Relief in UAE?

Revenue records for all tax periods since the business became a taxable person must be retained for at least seven years from the end of the relevant tax period. The FTA requires sufficient documentation to substantiate the revenue figures declared, including invoices, bank statements, and accounting ledgers. SBR does not reduce this record-keeping obligation.

Key Dates for Small Business Relief in UAE

- Available from: 1 June 2023

- Last eligible period end: 31 Dec 2026

- Election made on: EmaraTax return

- Revenue threshold: AED 3,000,000

- MNE Group threshold: AED 3.15 billion

Official References for Small Business Relief in UAE

[1] Article 21, Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses. Ministry of Finance, UAE. mof.gov.ae

[2] Ministerial Decision No. 73 of 2023 on Small Business Relief for the Purposes of Federal Decree-Law No. 47 of 2022. Ministry of Finance, UAE, 3 April 2023. mof.gov.ae

[3] Federal Tax Authority Corporate Tax Guide: Small Business Relief (CTGSBR1). FTA, August 2023. Available at tax.gov.ae

[4] Article 50, Federal Decree-Law No. 47 of 2022 (General Anti-Abuse Rule). Ministry of Finance, UAE.

[5] Ministerial Decision No. 97 of 2023 on Transfer Pricing Documentation Requirements. Ministry of Finance, UAE.

[6] Cabinet Decision No. 44 of 2020 on Organising Reports Submitted by Multinational Corporations. Cabinet of the UAE.

[7] Deloitte Middle East: “New Ministerial Decision Offers Relief for Small Businesses and Start-Ups.” 10 April 2023. deloitte.com

[8] Federal Tax Authority Corporate Tax Legislation Index. Full index of all Ministerial and Cabinet Decisions under the CT Law. tax.gov.ae

[9] Article 11, Federal Decree-Law No. 47 of 2022 (Definition of Resident Person). Ministry of Finance, UAE.

[10] Article 40, Federal Decree-Law No. 47 of 2022 (Tax Group provisions). Ministry of Finance, UAE.

[11] Ministerial Decision No. 134 of 2023 on General Rules for Determining Taxable Income. Ministry of Finance, UAE.

[12] Article 39, Federal Decree-Law No. 47 of 2022 (Tax Loss carry-forward, 75% cap per period). Ministry of Finance, UAE.